The Process of Bank Credit Creation

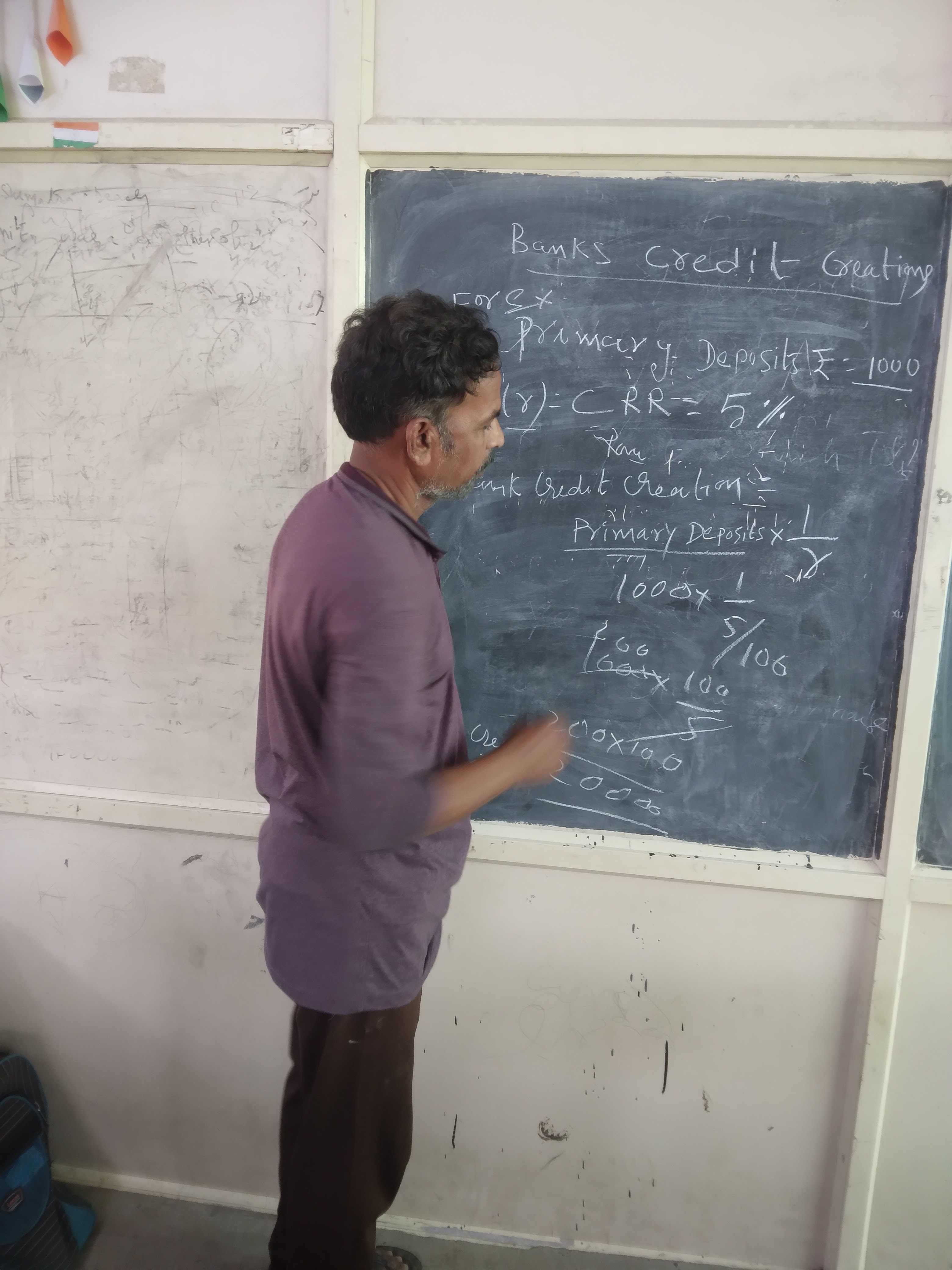

Bank credit creation is the lifeblood of modern economies. It's the process by which banks, acting as intermediaries between savers and borrowers, effectively "create" new money in the economy, fueling investment, consumption, and ultimately, economic growth. Understanding this process is crucial for anyone seeking to grasp the complexities of monetary policy, financial stability, and macroeconomic dynamics. While the concept might seem magical, it's rooted in a specific set of principles and constraints.

Bank credit creation is the lifeblood of modern economies. It's the process by which banks, acting as intermediaries between savers and borrowers, effectively "create" new money in the economy, fueling investment, consumption, and ultimately, economic growth. Understanding this process is crucial for anyone seeking to grasp the complexities of monetary policy, financial stability, and macroeconomic dynamics. While the concept might seem magical, it's rooted in a specific set of principles and constraints.

Demand for Loans: The multiplier effect only works if banks are willing to lend and borrowers are willing to borrow. If there is a lack of demand for loans, even with ample reserves, banks will simply hold onto the excess reserves, and the credit creation process stalls. Economic uncertainty, high interest rates, or lack of confidence in future prospects can all dampen loan demand.Bank's Willingness to Lend: Banks may choose to hold excess reserves even if loan demand is present. Factors influencing their lending decisions include perceived risk, regulatory scrutiny, capital adequacy ratios, and overall economic outlook. During times of crisis, banks tend to become more risk-averse and tighten lending standards, limiting credit creation.Public's Desire to Hold Cash: The multiplier effect assumes that all loaned money is redeposited into the banking system. However, individuals and businesses may choose to hold some of the money as cash. The higher the proportion of cash held outside the banking system, the smaller the money multiplier effect. This leakage from the system reduces the overall amount of credit created.Central Bank Policy: The central bank plays a crucial role in influencing credit creation through various monetary policy tools. Besides the reserve requirement, the central bank controls the money supply through open market operations (buying and selling government securities) and by setting the policy interest rate (e.g., the federal funds rate in the US). Lowering interest rates encourages borrowing and lending, while raising them has the opposite effect. The central bank also acts as the lender of last resort, providing liquidity to banks facing financial difficulties, which can help stabilize the financial system and encourage lending.

Inflation: Too much money chasing too few goods and services can lead to inflation, eroding the purchasing power of money and distorting economic decision-making.Asset Bubbles: Easy credit can fuel speculative investments in assets like real estate or stocks, creating asset bubbles. When these bubbles burst, they can lead to significant financial losses and economic downturns.Financial Instability: Excessive lending can lead to over-leveraging and risky lending practices, making the financial system more vulnerable to shocks. A sudden decline in asset values or a surge in defaults can trigger a financial crisis.Moral Hazard: The perception that the government will bail out banks in times of crisis (the "too big to fail" problem) can encourage excessive risk-taking by banks, leading to further instability.

Comments

Post a Comment